November 4, 2000. Don Quixote de Oro: El Abogado

Initial drafts of the remaining sections of my memo are now posted at BIS: Bank for Intervention and Subversion. Many thanks to those who have responded to this new site feature with contributions to GATA. Thanks, too, to all who have sent me e-mails with comments and suggestions. Some will find evidence of their input in the new materials just posted, proving again that two heads are often better than one. Also appreciated are the several expressions of concern about my personal safety, although in this context that is a matter largely outside my control.

Of all the e-mails that I received on the BIS project, the most difficult to answer put the following question: "What is the minimum that GATA must raise to launch the suit?" I answered:

There is no right answer to the question. In any legal attack of the sort that GATA contemplates, the other side will spend millions. What will it take to wage an effective battle against that? I don't know. I think that GATA's target of $100,000 is appropriate for the time being. However, that amount is less than the annual starting salary for a first year associate at a big law firm in Boston today. So in that sense, $100,000 is kind of like one rookie ball player taking on the New York Yankees. But then, David did beat Goliath. It's just not the way to bet. My role is to help Bill Murphy and GATA do the best they can with whatever funds they can raise. The more they raise, the better the show we can put on.

But money is not the only requirement. Information -- people willing to come forward and testify to relevant facts or provide relevant data or documents -- is just as important if not more so. Many can give money. Only a few can or will give critical evidence. The gold cabal has declared war on free markets, free governments and the Constitution itself, but the cabal has yet to produce a John Dean.

By now, regular visitors to The Golden Sextant must know that Daniel Webster ranks high on my list of heroes. The Millennial Candidate, my project in the realm of fiction, is necessarily on hold. But as our intrepid band of GATA supporters and gold bugs goes forward on the BIS project, and whatever the result, there will be a reward on which no price can be put, in gold or dollars. In the only capital case that he ever prosecuted, a murder trial that ranked as the O.J. case of its day, Daniel Webster concluded his closing argument to the jury with these words:

There is no evil that we cannot either face or fly from, but the consciousness of duty disregarded. A sense of duty pursues us ever. It is omnipresent, like the Deity. If we take to ourselves the wings of the morning, and dwell in the uttermost parts of the sea, duty performed, or duty violated, is still with us, for our happiness or our misery. If we say the darkness shall cover us, in the darkness as in the light our obligations are yet with us. We cannot escape their power, nor fly from their presence. They are with us in this life, will be with us at its close; and in that scene of inconceivable solemnity, which lies yet further onward, we shall still find ourselves surrounded by the consciousness of duty, to pain us wherever it has been violated, and to console us so far as God may have given us grace to perform it.

October 27, 2000. The BIS and Greenspan: Freezing-Out the U.S. Constitution

With this commentary, The Golden Sextant introduces another new site feature: BIS: Bank for Intervention and Subversion. Today, with the U.S. Federal Reserve occupying and voting its two board seats at the Bank for International Settlements, both intervention in the gold market for the purpose of affecting prices and acts in subversion of the U.S. Constitution are prohibited activities for both organizations.

This new project will focus on the recently announced plan of the BIS to freeze-out its private shareholders at an Extraordinary General Meeting scheduled for January 8, 2001. The proprietor owns several shares of the American tranche, making this matter one of financial as well as academic interest to him. Other shareholders are advised to seek their own counsel. All opinions expressed here are those of the proprietor. No assurance can be given that they will be accepted or upheld by any particular court or tribunal.

Gold bugs have long considered the BIS an ally. Its shares, which pay a decent annual dividend, tend to trade in line with gold prices, making them an attractive proxy for bullion or mining shares. But accumulating evidence, to which the proposed freeze-out adds an important new dimension, suggests that for the past five years the BIS, with the active support of the U.S. Federal Reserve, has played a central role in trying to replicate the London Gold Pool of the 1960's.

Until 1994, the BIS functioned as the principal organization for cooperation among Europe's major central banks, of which several were and remain friendly toward gold. But with the signing of the Treaty of Maastricht in 1993, and the formation on January 1, 1994, of the European Monetary Institute, a predecessor organization to the European Central Bank, the BIS faced the prospect of playing a rapidly shrinking role in European monetary affairs. Then, reversing almost 65 years of prior official non-involvement, the Fed in September 1994 decided to occupy the two seats on the BIS's board to which the American tranche entitled it.

Shortly thereafter the BIS agreed to provide US$10 billion for the Mexican bailout effected mostly with funds from the U.S. Exchange Stabilization Fund. Since then, the BIS has been heavily involved in establishing reporting requirements and bank capital adequacy standards for derivatives. Their recent use to manipulate gold prices is the subject of many prior commentaries at The Golden Sextant. The BIS has also sought to expand its activities beyond Europe by opening an office for Asia and the Pacific in Hong Kong in July 1998.

According to reliable anecdotal reports received by GATA, the BIS worked closely with the Fed and the Bank of England to halt and then to reverse the rally in gold prices triggered by announcement of the Washington Agreement in the fall of 1999. Indeed, a careful review of reports in the European press about the genesis of the agreement suggests that BIS officials may have been deliberately excluded from the negotiations along with the Americans and the British. In any event, by supporting the Anglo-American response to the Washington Agreement, the BIS seems to have turned on its most important European members.

When the Fed took its two board seats at the Basle-based bank in 1994, the event passed almost unnoticed. There were no congressional hearings. Nor was there any public statement by the President or the Secretary of State. Indeed, so far as I can determine, there is no record of any approval or assent to the Fed's action by the Department of State. Its silence on the matter is particularly odd. When the BIS was formed in 1930, then Secretary of State Henry L. Stimson expressly and publicly prohibited the Fed from participating, directly or indirectly, in the affairs of the BIS.

The Fed's decision in 1994 was reported in an article by C. J. Siegman, "The Bank for International Settlements and the Federal Reserve," Federal Reserve Bulletin, October 1994, p. 900 ff. This article is an important resource, but contains no mention of any legal authority or permission for the Fed's formal participation in the BIS. Not until almost a year later did The New York Times in a story by K. Bradsher, "Obscure Global Bank Moves Into the Light," August 5, 1995, Business, p. 1, report that the Fed had "joined" the BIS.

As the story noted: "[T]he bank is beginning to draw the attention of the same unlikely array of American populists who have opposed the new World Trade Organization." It continued: "Mr. [Ralph] Nader objects to the bank's unusual independence under international law, including an exemption from many Swiss laws. 'It is outside the rule of law,' he said. 'It's above the law.'"

Mr. Nader has a point. If the BIS is indeed intervening in the gold market, either directly or on behalf of its member central banks, it is operating in opposition to current U.S. law mandating a free gold market. What is more, there are serious constitutional issues with respect to whether the Fed had authority to take its two board seats without more formal authorization from the President and the Congress. Should the freeze-out be effected, these issues become even more troublesome for the Fed.

Legal and constitutional issues of this nature are frequently difficult for private parties to raise due to lack of standing. That is, there is a general principle of law that in order to complain in court of legal or constitutional wrongs, parties must have some direct pecuniary or other interest beyond that of all citizens in seeing that the laws and the Constitution are enforced. By attempting to freeze-out its private shareholders, the BIS has opened the door to potential litigation by private parties who by virtue of holding BIS shares have standing to raise any issue directly affecting the value or ownership of their shares.

Precisely why the BIS has elected to run this risk of litigation is unclear. One possibility is that it is planning certain activities that it does not want to reveal publicly through its financial reports, such as buying or selling gold for its own account or engaging in substantial new gold lending for its central bank clients. In this connection, it can perhaps be argued that gold deposits by central banks at the BIS are not ordinary gold lending, thereby enabling organizations with prohibitions on gold lending, such as the International Monetary Fund, to permit some of their gold to reach the market through the BIS without clearly violating their own rules.

Under Article 54(1) of the Statutes of the BIS, disputes between it and its shareholders "with regard to the interpretation or application of the Statutes of the Bank...shall be referred for final decision to the Tribunal provided for by the Hague Agreement of January, 1930." This reference is to an arbitration tribunal established under Article XV of the Agreement between Germany et als. Regarding the Complete and Final Settlement of the Question of Reparations, signed at The Hague on January 20, 1930, 104 League of Nations - Treaty Series (1930) No. 2394. The United States is not a signatory to this treaty, which it pointedly refused to enter. The arbitration provision provides in relevant part (104 L.N.T.S. 252-253):

1. Any dispute, whether between the Governments signatory to the present Agreement or between one or more of those Governments and the Bank for International Settlements, as to the interpretation or application of the New Plan shall ... be submitted for final decision to an arbitration tribunal of five members appointed for five years ....

9. The present provisions shall be duly accepted by the Bank for the settlement of any dispute which may arise between it and one or more of the signatory Governments as to the interpretation or application of its Statutes or the New Plan.

The so-called "New Plan" for payment by Germany of war reparations arising out of World War I ended long ago, and with it any justification for the continued existence of the arbitration tribunal, which under the treaty had a mandate only to hear disputes between the BIS and signatory governments, not between the BIS and its shareholders. Perhaps when the tribunal was in existence a claim could have been sustained that it possessed appropriate ancillary jurisdiction over such disputes. But to recreate this tribunal today to hear a dispute not covered by the treaty seems a big stretch.

While U.S. courts regularly honor agreements to arbitrate, it is difficult to order arbitration before a tribunal that no longer exists. Conceivably an argument could be made that the Permanent Court of Arbitration at the Hague should form a tribunal to substitute for that originally contemplated. Indeed, it is rather surprising that the BIS did not long ago update Article 54(1) along these lines. The PCA has a modern set of rules for arbitration between international organizations and private parties. Of course, even now this alternative is one to which all parties could agree.

But without a creative judicial order or a voluntary agreement to arbitrate, the BIS could well find itself a party defendant in a U.S. court. The United States is not a party to any of the international agreements or conventions relating to the BIS, undercutting any claims that it might assert to immunity here. In the case of any proceedings to challenge the freeze-out brought by American citizens who own shares of the American tranche, strong arguments can be made for jurisdiction in U.S. courts, particularly if the Fed or its officials are made parties defendant in addition to the BIS. Indeed, the presence of important questions of U.S. constitutional law makes an American court in many ways the most appropriate forum.

The principal purpose of this new site feature is to give other private shareholders of the BIS access to some of my research and analysis as I wrestle with the problem of how to respond to the freeze-out. Because the freeze-out raises important constitutional issues affecting the conduct of both monetary and foreign policy by the United States, many who are not private shareholders may also be interested. What is more, any litigation between the BIS and its private shareholders is likely to focus considerable scrutiny on recent official efforts to manipulate gold prices, especially through the use of derivatives. For this reason, GATA is considering whether to support this project as a follow-up effort to its Gold Derivative Banking Crisis, a document that has now been downloaded over 20,000 times.

For the next month, this project will be very much a work in progress. Readers should be guided accordingly. Currently, as indicated by the contents directory, the finished memorandum is projected to contain ten chapters or subparts. Initial or partial drafts of the first nine are being posted at the same time as this commentary, and the tenth will begin to appear in due course. All are subject to revision and enlargement as appropriate. Notations on the current status of each subpart will also appear in brackets in the contents directory. This procedure is not ideal, but seems under the circumstances to be the most efficient way to get as much material as possible posted quickly while allowing good opportunity for useful and timely reader input.

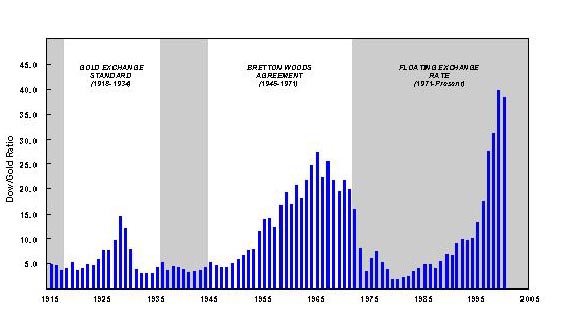

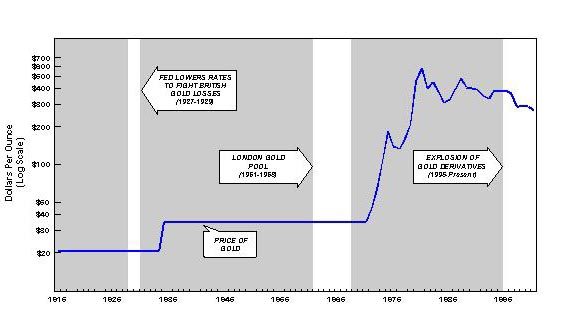

October 17, 2000. The Dow/Gold Ratio and the International Monetary Order

The two charts below, reproduced with permission of Golden Sextant Advisors LLC, portray the Dow/Gold ratio in relation to the international monetary regimes of the past century and the coordinated official interventions in the gold market that marked the beginning of the end for the gold exchange standard and the Bretton Woods system. Great bull markets float not on a sea of easy domestic credit, but an ocean of international liquidity. Gold is best seized at the flood, when Anglo-American governments lead the campaign to denigrate its value in a vain effort to escape its discipline.

For a discussion of the Dow/Gold ratio, see Dow/Gold Ratio = 1 at $3000: Don't Laugh!. For a bit of irony, read Fed Chairman Alan Greenspan's account of the Fed's decision in 1927 to lower interest rates in his 1966 essay "Gold and Economic Freedom" (reprinted in A. Rand, Capitalism: The Unknown Ideal), and quoted in part in Collision Course: Gold and Greenspan.

October 8, 2000. Charting the Gold Markets: Regressing to ?

Since the last commentary, there have been more tremors, the most noteworthy being the coordinated intervention in support of the euro just before the G-7 meeting in Prague. A few days later, the Frankfurter Allgemeine Zeitung published allegations, subsequently denied by Citibank, that it had received advance word of the intervention through former U.S. treasury secretary Robert Rubin, now a Citibank executive. What is more, the FAZ story went on to suggest that Citibank used this knowledge to front-run the intervention, thereby blunting its effect. Apparently the Bundesbank was blowing off more steam through its favorite newspaper.

Geologists trying to give useful early warnings of earthquakes do not confine themselves to watching the odd behavior of snakes. Today there are high-tech instruments to measure premonitory signs and signals of impending seismological events. In the financial world, too, modern technology provides new predictive techniques. So, in addition to continuing to keep close tabs on the financial snakes, The Golden Sextant is adding a new feature: regularly updated regression analyses of publicly reported key data on certain gold and gold derivatives markets.

The analyst working with me on this project is G. Michael Bolser, a fellow GATA supporter. Mike, a former military flight instructor, is an optical physics developer. He has also worked in the medical diagnostics and coronary laser fields. With a background in mathematics and an interest in gold, Mike enjoys doing regression analyses of various segments of the gold market, and has very kindly offered to share his hobby with others in the gold community through my website.

Regression analysis is a tool more familiar to younger people who have grown up using computers than to us older folk who recall plotting quadratic equations by hand in algebra class. To review: a linear equation (i.e., y = x + 2) gives a straight line when graphed; a quadratic equation (i.e., y = x^2 + 1) usually gives a parabola, but may give an ellipse, hyperbola or a circle. Polynomial equations of higher "orders" (up to six terms) yield more complex curves.

But just as an equation can be plotted on a graph, a series of data points on a graph can -- particularly when they suggest a line or curve of some sort -- be assigned one or more equations that when plotted will appear to replicate to a greater or lesser extent the same pattern as the plotted data. If the equation perfectly captures every plotted data point, its regression squared (R^2) value is 1. If the data were completely random with no pattern, the R^2 value would be zero. In practice, R^2 values greater than .5 are usually considered indicative of a pattern that may have some predictive value.

Because the plotted data has been assigned a mathematical formula, the formula itself can be used to calculate projected data points. Thus, if many data points plotted over a long period of time fit very closely a line or curve expressed by a specific mathematical formula, the formula will have a high R^2 value and can be used to plot with some degree of confidence future or projected data points for short intervals. In addition to its predictive value, regression analysis by sharpening existing data patterns can sometimes shed further light on the underlying processes at work as well as indicate things to watch for that might have significance.

Several cautions are in order. First, mathematical formulas are used to generate a line or curve that best fits the given data. These formulas do not express the underlying processes being studied except as they capture the pattern of the data. Second, with data plotted over time sequences, the date selected for commencement of the plot affects -- sometimes quite dramatically -- the pattern, and therefore the R^2 values and the curve's fidelity to the underlying data. Third, as projected data is replaced by actual data, choices must be made with respect to continuing the regression analysis with the original formula or updating it with a new formula taking account of the new actual data. In general, as new data is added, a rising R^2 value confirms the original assumed regression line, while a falling R^2 reduces its predictive utility.

The charts, as revised and updated, are posted at GOLD MARKET REGRESSION CHARTS.